When the Curve Flattens

Trade With Titans 1 — 8/6/24

In yesterday’s post, I mentioned that I was planning on doing more trading-related content and flexing those muscles again. I’ve been chatting with my longtime friends at Trade With Titans and decided to help out with their content revamp, where I’ll be aiming to write a few “market insight” newsletters on a regular basis. As opposed to the native posts on this site, I’m aiming for insights that, while not directly actionable, are geared towards the burgeoning trader (which I think overlaps with quite a bit of readership here), and hopefully provides a pathway for readers to incorporate my way of quantifying-but-not-quanting way of interpreting markets, even if just for fun. Trust me, even if you don’t trade, you’ll sound like a genius at happy hour.

These posts will come on their newsletter first — on weeknights, of course, so there’s time to read it before the following trading day — along with some other goodies, such as their latest levels, bot updates, and other educational content they have prepared. You can sign up for free here:

I will, of course, post what I’ve written on here on the following morning that doesn’t already have my own native post scheduled to send. I’ll also put the topic tags as a heading, for easy keyword search in the archive ( https://maltliquidity.substack.com/archive ) as reference points. Without further ado:

On: Macro, VIX term structure, Volatility

In the past couple days, we’ve probably heard the phrase “yen carry trade” more than we care to admit. And certainly, plenty of us have at least watched, if not traded, /6j ourselves. But does it really make sense to attribute a massive selloff in US equities, across the board, to a 25 bips hike from July 31st? Instead of attributing narratives to move, I’ll give some perspective on how I analyzed the move in real time, and how I think about the interplay between global macro and intraday trading.

On Sunday evening, when I first started seeing futures sell off , I was a bit skeptical of the immediate attribution to Japan. It simply didn’t make sense to be hitting NQ/ES on the Nikkei move — and, frankly, USD/JPY has been dropping for a month straight — on July 10, it was above 160 per. What would have made someone specifically unwind a “yen carry trade” to such a massive degree that it takes down the entire global market? It just doesn’t add up on face value.

However, there is something to note in that Sunday night is by far the most illiquid overnight session of index futures, and on top of that, NQ is significantly more illiquid than ES. After all, the Nasdaq-100 is composed of primarily the biggest tech stocks that we all know that also see some of the heaviest equity options flow in the market — something that overnight delta one volume just doesn’t match up to. If you did want to sell through an illiquid book, you’d choose Sunday night to do so. But why would someone purposely want to shred the markets down? Well, it’s no secret that VIX generally spikes when the market sells off — it has an inverse relationship with price. If someone accumulated a position over the past couple weeks tethered to the VIX, it would make sense to try and spike the print due to the exponential nature of the movement, and a potential payout.

This isn’t exactly without precedent. Especially in the low-volatility years prior to 2020, it was theorized that VIX settlements could be manipulated through zero-bid options to “set” a print. Indeed, you saw a batch of litigation surrounding the infamous “volpocalypse” XIV blowup of 2018 that forever changed how inverse volatility products worked with the market. While the litigation took ~5 years to resolve, the point remains that the market still can react to such a print. If you have a position that pays off on a high VIX print startling the market in one way or another, you either need a global pandemic, a global recession, or an illiquid market with a changing volatility regime with a soft book. Indeed, the VIX print Sunday night was the third highest since 2008, with only 1 COVID print that outdid it.

It makes sense to look at what exactly VIX is, though — while ostensibly a “volatility index”, it’s not exactly volatility itself, is it? While it’s calculated off index options, it stands to reason that the real-time trading activity of those options might differ from the calculation spit out in real-time. And when options aren’t really trading on a Sunday night… well, you get where I’m going with this.

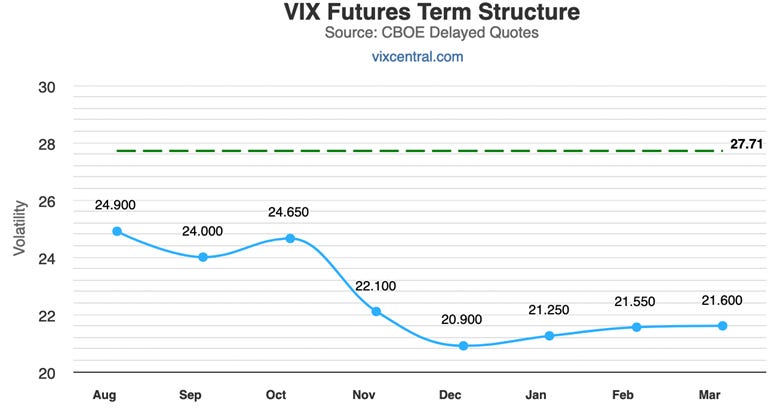

Take a look at the VIX term structure on one of my favorite sites, vixcentral.com. (Seriously, bookmark this link — one you absolutely should look at regularly.) You can peruse through the site’s help function and other explainers of VIX futures, contango, backwardation, but at a glance, we should be able to figure out what’s going on pretty easily:

The current term structure implies elevated volatility for the months of August, September, and October, and a dampening after the election in November. Now check the curve from July 22:

At the time, I wrote that

given that we still don’t know at time of writing why the sitting president fired himself by Twitter post, which nobody has explained yet, overall vol seems underpriced. This isn’t necessarily bad for stocks — as we all know, stocks don’t really move along political news (trade talks going well) — I think it’s a rare overall directionless vol trade. But from a macro perspective, the consideration shifts. With Harris as the presumptive nominee, her odds will be reflected by the yield curve and DXY movement…

(yes, I’ll be continuing to refer back to my old posts, in the nested style that really needs a better way to peruse — I’m working on it! ~ed.)

By Wednesday (July 24), the curve had steepened further — and with vol curve expansions, we naturally start to expect more intraday reversals, currency movement (given the macro environment), and outright selloffs. Indeed, on that Wednesday, we had the first 2% selloff all year, and, of course, our 25 bips Japan rate hike just one week later. There was a lot going on and a lot to price in, and I remarked multiple times that it still seemed a bit too low. Note that there’s nothing inherently illegal about selling through a book that lacks sufficient depth to eat your order (not legal advice, of course), as this is precisely why we tend to use limit orders instead of market orders. But there are situations where you might be biased towards one price print over another — an obvious scenario that comes to mind is at option expiry, where there might not be any practical difference from a profit point-of-view when an equity option expires .01 ITM as opposed to OTM, but from a practical point of view, it certainly is an annoyance where the ITM expiry ties up the underlying shares as settlement gets resolved!

I have no way to confirm this, of course, but if I had to guess, this is probably what caused the “tape bomb” of Sunday night, along with some cascading liquidations in crypto movement (no idea what the catalyst was there — there were some margin change requirements I saw, but I find it hard to fathom that it took BTC/ETH down so much off what was likely a telegraphed change.)

It's also why, after seeing the 60 VIX print and a pretty tepid day trading after, I was pretty convinced we’d revert upwards.

I remarked to a friend, “Think back to COVID — did that seem like a true 60 VIX print to you?”

There’s no way to confirm this theory of course, but just like vol tends to spike on the way down, compression tends to correlate with upside. Certainly, the Nikkei entirely retracing the drop played some role in assuaging “fears”, but there’s no way to really know in real time what the “cause” of each move is — instead, a better modus operandi is to not get obsessed with the narratives of “carry trade blowing up” and “emergency rate cuts”, or whatever is blowing up the “For You”/financial media algorithms, to avoid making an irrational, emotional decision in favor of utilizing the levels and tools in front of you. Sometimes you just have to ask yourself, “does this make sense?”, and prevent yourself from getting too attached to one side or another and stay within your risk limits.

Note: this definitely overlaps with my prior ML post, but I didn’t get to go into the VIX term structure mechanics I’ve been eyeballing for a while now.

And just for fun, here’s a really silly tip that happens to work ludicrously well that I alluded to the other day:

Sometimes it really is this simple.

Anyway, I’m aiming to have 1-2 of these TWT posts up a week. As usual, my thoughts will be free to read.

A note on “affiliated content”:

At the moment, I do not have any “direct” deal with TWT, for referrals or otherwise. I don’t use any signals to trade myself. I have worked with a couple of the main individuals involved to build automated trading strategies in the past, completely independent of any subscription service (I have never sold a sub in my life), and enjoy talking to them about markets frequently. I truly do just do this because I enjoy it and like the conversation and interactions it drives — it’s not a coincidence I started writing publicly ~3.5 years ago when Money Stuff was on break. After all, I taught myself finance through Levine’s free newsletter, and I’d like to maintain that ethos. That being said, “content” does merge a lot with my own interests going forward, both as personal record-keeping and part of future business interests, and it’s a good way to allow myself to keep myself sharp with regards to markets without having to watch tickers and trade every single day. Thanks again for reading, I really appreciate it — if you do find this type of stuff useful, I’d appreciate a forward/share.