THE FUTURE OF FINANCE

Reframing risk for the Artificial Intelligence age

If you asked me to define finance, I’d call it a philosophy centered around the interpretation and quantification of risk. From there the risk can be chopped up, transformed, absorbed, ignored, or reimagined in a nearly endless manner.

And that’s where my concept of “liquidity theory” comes from. By boiling down this system to three core elements — equity, currency, and debt —

Equity provides liquidity to hope. Currency provides liquidity to bargaining — our transactions have to be denominated in something. The most important pillar, and what underpins it all, is debt, which provides liquidity to trust. The systems of law and government provide a safeguard of enforcement to trust, but trust without liquidity cannot scale — there is no society without it.

we can interpret the past actions of humans and speculate on the future to better anticipate risk and increase the likelihood of positive outcomes.

While I’ve always thought this definition was succinct, I’ve also felt slightly disconcerted the entire time, because it’s not exactly rigorous. It’s unclear how the world of spreadsheets, signals, banks, and companies interact as a direct construction from these concepts. And certainly it’s immensely profitable to even capture a slice of the systems developed to interpret finance as a whole, but in the modern era, we should be able to do better than automated trading and constrained-universe modeling.

Fortunately, my good friends from Alphafund have come up with the novel concept of Economic World Models (EWM) to bridge this gap.

The core insight of the EWM approach is that, instead of interpreting risk through a core denomination, such as dollars, all risk is envisioned as a function of capital flowing through the global economy through intelligent systems called corporations.

The corporation isn’t a specific type of business; rather, it’s a set of constraints to be optimized over time, with the goal of continued existence and increased data absorption creating a self-sustaining, recursively improving system.

This is a neat solution to a core problem I have with modern financial modeling — it shouldn’t be necessary to split interpretations into industry-specific categories so financial analysts can opine on outcomes through glorified blog posts. The EWM is the dynamically adjusting model that won’t, for example, chase stock price movement to retrofit price action to an already-existing spreadsheet template.

Notably, this avoids an LLM-based approach, which has serious constraints in the method it makes predictions and its lossiness when taking in forward data. LLMs are constantly retrained on future information, which creates a sort of post-hoc rationalization effect that muddies up a dynamic system and introduces a lot of noise. An EWM only operates in a forward timeline dependent on the continued existence of the corporation, dynamically adjusting to incoming data, but not retrofitting explanations to “correct” prior adjustments. Essentially, it avoids the classic “article that explains the previous day’s price action, but is useless making forward predictions” problem that journalism has.

Applications

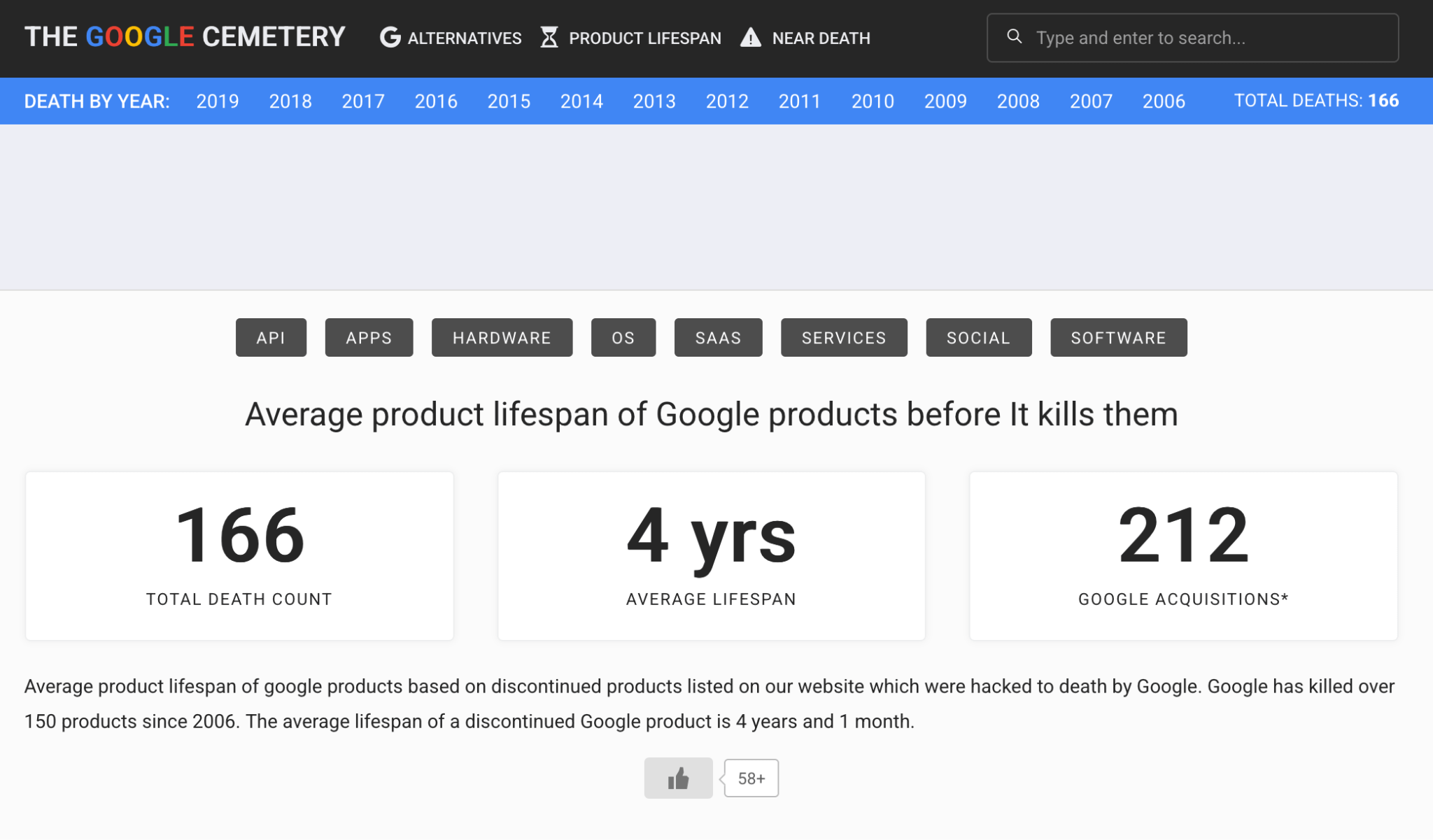

Part of the reason I got so excited when I first heard this concept is that it squares away a big issue I have with how large-scale businesses are run. For example, take a gander at the infamous Google cemetery.

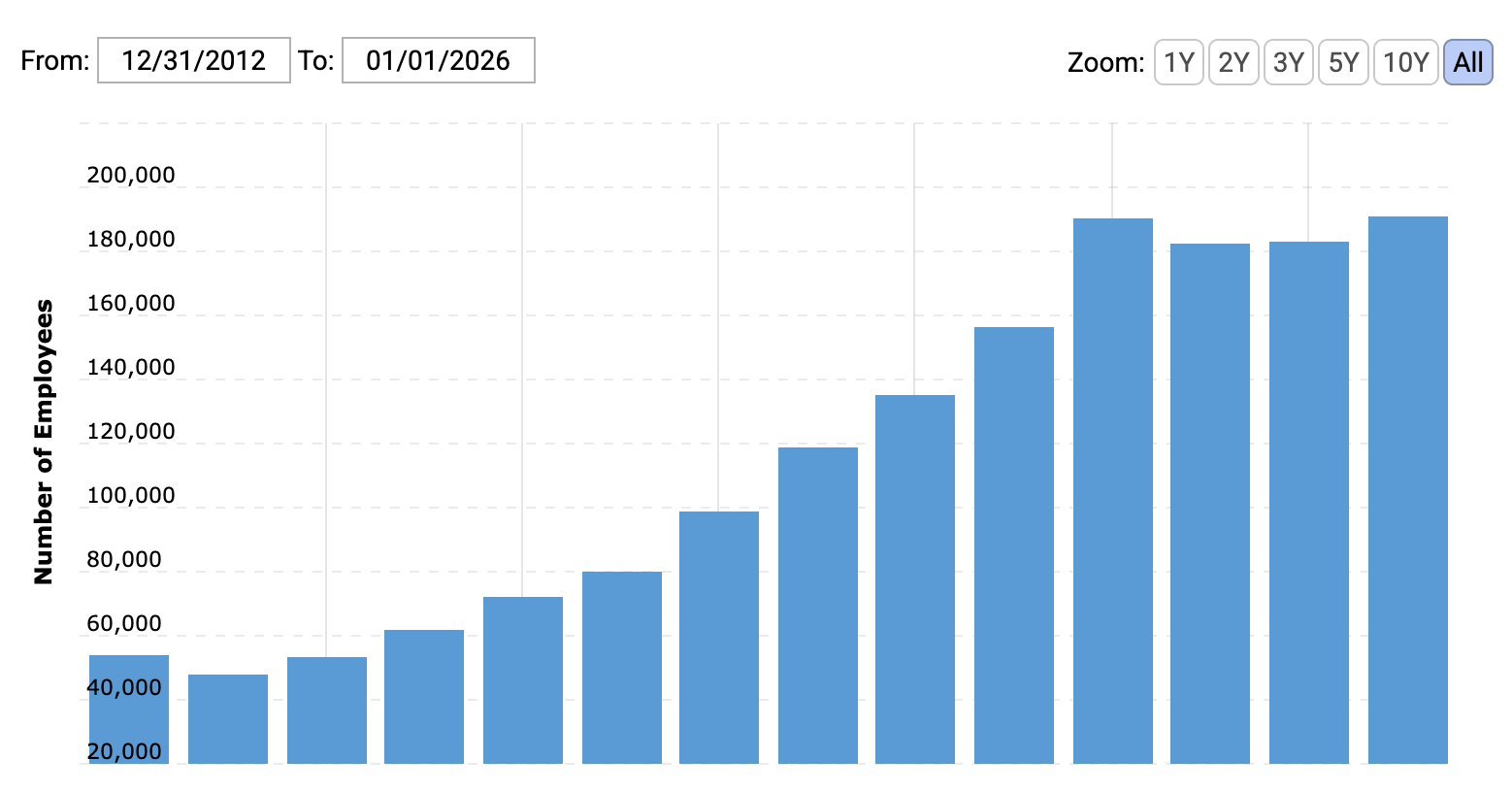

While Google could arguably have reached the pinnacle of corporate influence, it’s not a controversial take to say that, for many years, capital allocation was rather aimless. Throughout the 2010s, while looking for a new corporate direction beyond search, Google acquired hundreds of products, hired tens of thousands of employees, yet very little of this capital allocation was efficient.

Of course, a lot of this panned out, given the current state of TPU research, Deepmind, Gemini, and more. But this highlights a problem far beyond stock price prediction that EWMs solve. Google is an organization that simply scaled beyond human coordination. A corporation, practically speaking, is a combination of two separate-but-related problems: running a core business, and properly allocating excess capital. Traditionally, these problems are handled by different divisions. In the case of Google, management of “search” is split from management of “maps” with the capital being aggregated and allocated to the “human capital” division and the “venture” division. Each step that segments the overall system creates friction, redundancies, and obsolescence. All of these divisions exist in the same matrix composed of “properties of the Google corporation”, yet the hapless corporate finance division is forced to look at quarterly snapshots to make forward allocation decisions. This should be a real time, continuous process!

This is a problem that quantitative finance solved. When the corporation’s main objective is optimal allocation efficiency, the only real concerns are execution quality and avoiding redundancies. This is where the pod shop model of hedge funds originated from: centralize all the strategies in one main shop, have a centralized risk book to prevent pods from inducing too much positive or negative correlation, have hard risk limits, and over time you can’t really lose unless a human meddles with the weights, as seen in the infamous Two Sigma case:

The researcher manipulated the firm’s models in an attempt to boost his compensation, and the changes led to unexpected gains and losses of $620 million across its funds, the report, which cited people familiar with the matter and letters sent to investors, said. The changes the researcher made led to $450 million of gains in funds where employees invest alongside external investors, and losses of $170 million largely borne by clients, the Journal said.

Google is not stupid. Acknowledging the difficulties of allocating the forward cash flow from their money printer, they do allocate to a plethora of different funds running uncorrelated strategies, and avoid blasting billions of dollars into a failing golf league. (The Google cemetery is clearly a relic of the 2010s, given how much nonsense has proliferated since then. Just doesn’t hit the same.) But therein lies the limitations of non-EWM predictive models — multistrat firms have already scaled to critical mass, and running specific strategies has a hard cap on theoretical AUM, as allocating past what the market supports would destroy returns due to outsized price impact.

The EWM, on the other hand, works better internally rather than externally. If the base constraints of the corporation are properly constructed initially, what emerges is a kind of super-CFO — a bridge between the core business and the capital allocation, where unique data internal to the corporation can be loaded over time to better synchronize the management of core business risks and overall macroeconomic risk. After all, there’s no such thing as a business that operates in a total vacuum. Theoretically, a firm with a properly constructed EWM could scale out and through rather than “up” by maximizing AUM. And, of course, as is the case for all massive scale machine learning models, the more unique training data that can be internalized, the better the predictive power gets.

Implications

The classic attraction to machine learning methods over efficient algorithms is the scaling argument. Machine learning improvement is exponential as the amount of (clean) data ingested increases, while algorithms definitionally have capped efficiency. And while this is data dependent (as all things are, for that matter),

EWMs have a unique advantage over other prediction approaches — namely, that profit and loss is organically noise-filtering. What’s particularly delightful is that the machine approach is the exact one I undertook when I decided to trade, rather than work a corporate job:

Everything I have done, in a sense, has been towards figuring out that question of “why we ask why” — which logically extends to “why do we trade”. In grade school, I was known for correcting my teachers incessantly, and when told to just do my work, this discontentment never left. The areas I mastered: chess, intensive pattern recognition so we know that we are speculating with confidence, math, rigorous formal logic that attempts to quantify and codify the infinite, and trading, testing my theories and being validated by profit, all reflect a different way of trying to solve that question.

The tricky part about any machine learning model is that, when you are iterating through trillions of parameters, even a 99.999% accurate signal will amplify a ton of noise. And, of course, there are filtering techniques that help with this. But if the data is clean — pure signal — the less the output is influenced. Amazon is perhaps the best example of an owner of perfectly clean data. When you go on the site, or click on an ad, they have end-to-end control of every metric that could be generated from start to finish — purchase probability, return %, etc. — from which a near-perfect recommendation algorithm can be generated. Even someone like Meta, one of the most efficient ingesters of user data on the planet, has a bit of loss in their signal — since they can’t truly confirm whether you purchased anything from clicking on an ad, there is a tiny bit of noise at the endpoint where you leave to Sun Day Red’s website to buy a Cosmic Blue Jacquard polo before it sells out.

In a complex system, profit and loss is about as good as you can get. For example, if I lose money on a trade, I know there’s something that went wrong and internally can adjust my behavior upon further analysis. If I make money on a trade, it’s not a one-to-one signal that I was correct, but it’s a positive direction to index on when looking to make trades in the future.

Why wouldn’t this work exactly the same way with an EWM, but at a much larger scale?

Scaling

Largely, I think this is the core view that generates “finance as a philosophy”. If one truly believes in their viewpoints, one would bet on it, either by adjusting their life circumstances, risking their personal capital, or risking their reputation. It doesn’t need to be dollar-denominated in the human world — simply allowing your ideas to stand on their own merit, rather than referring to credentials, is a form of betting on what you believe in. “Skin in the game”, as Nassim Taleb would put it.

The goal of the EWM approach, as I’ve interpreted it, is to hyperscale this philosophy. The more universes that are ingested, and the more predictions that are made, the PnL of the corporation object forms a trajectory like a particle mapping a surface in physics — a turbocharged version of the idea behind applying geometric brownian motion to model stock price movement, where the scaling factor occurs as the drift touches on balance sheets, economic cycles, private placements, and more. Most importantly, an EWM does not operate independently of capital concerns. The philosophy of raising as much money as possible for compute to train as large a model as possible and justify it through “well, the future applications will justify the spend” is not possible if the EWM is constructed properly — because the entire point is that profit is the signal. As I like to joke, what kind of trader wants to lose money? The entirety of the 2010s tech sphere is a kind of bizarro land, where the inverse logic of “lose money to scale” only works in a zero rate environment implying zero risk. Which, of course, cannot be possible in a financial system with any velocity whatsoever.

This could, for example, manifest itself as a self-managing corporation in the ideal state. Imagine an EWM that could decide for itself whether to allocate capital to training a better iteration of it, or allocating in a different manner to generate the capital to retrain later. So much of the discourse is obsessed with recursive intelligence machines — I’m much more excited about recursive money machines, because that’s the only way a model will ever contextualize how humans interact at scale. As Citizens United told us, corporations are people too.

To learn more about Alphafund, follow the link, check out Massey on twitter, or email contact@alphafund.com

> The tricky part about any machine learning model is that, when you are iterating through trillions of parameters, even a 99.999% accurate signal will amplify a ton of noise.

Reminds me of Friedrich Hayek's idea about information in The Use of Knowledge in Society. Once you have the full data, it's just a matter of applying logic to find the best strategy. Gathering the data is the hard part.

>In a complex system, profit and loss is about as good as you can get.

I think this is one reason prediction markets are particularly interesting. Check out some of the companies building prediction bots using LLMs like Mantic. Prediction markets need to resolve, so they provide a fairly clean signal, unlike price movements of stocks.

>The philosophy of raising as much money as possible for compute to train as large a model as possible and justify it through “well, the future applications will justify the spend” is not possible if the EWM is constructed properly — because the entire point is that profit is the signal.

If that's the case, how would wacky, out-of-distribution ideas be funded, like the internet or EVs? I'm sure the EWM's search space would've eventually led to the discovery of some signal showing that the internet could be useful, but I would think this would've taken a much longer time to uncover vs. someone saying fuck it and building it out.